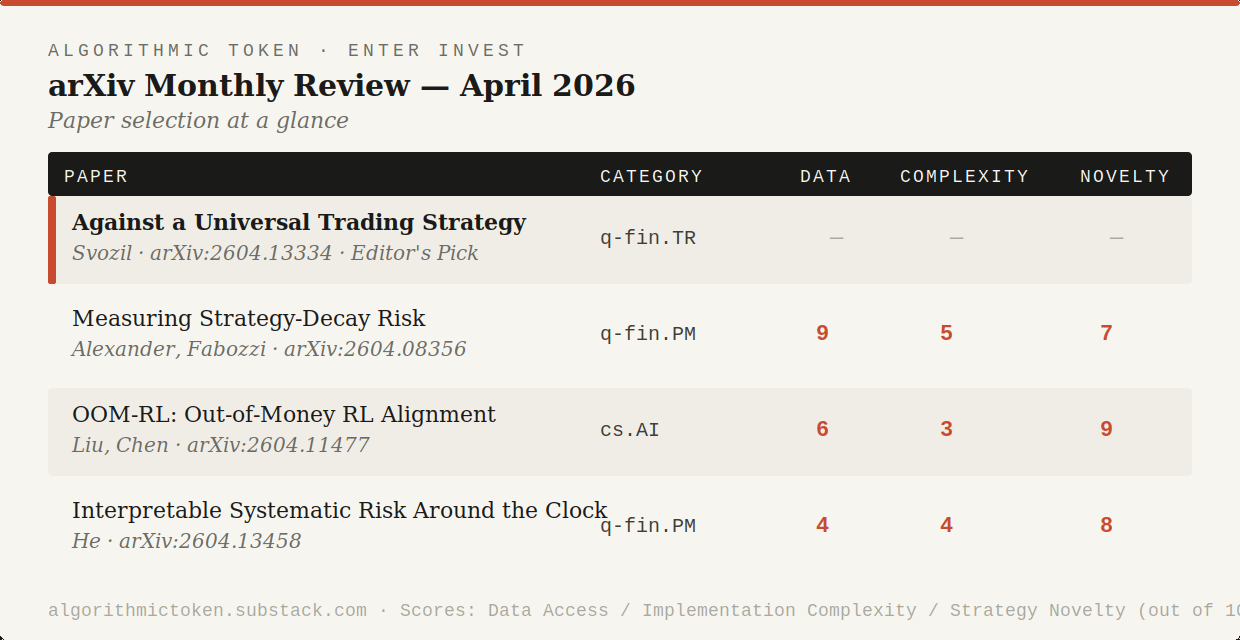

Algorithmic Token ArXiv Monthly Review — April 2026

Algorithmic Token · ENTER Invest · arXiv Monthly Review. Co-written, reviewed and edited by Nuno Edgar Nunes Fernandes April 30, 2026

A Note on the Monthly Review

This is the first edition of the arXiv Monthly Review at Algorithmic Token. Each month, on the last week of the month, we scan the quantitative finance corpus on arXiv — primarily from the q-fin.TR, q-fin.PM, q-fin.ST, and q-fin.CP sections, with cross-listings from cs.AI and cs.LG — and select the papers we believe are most relevant to practitioners in systematic and algorithmic trading. We may also add other similar quantitative finance literature sources to this monthly review, of which we reference its origin.

Our selection criteria are intentionally narrow. We are not trying to cover everything. We look for papers that propose testable signals or mechanisms, include empirical results on realistic market data, and where the methodology is implementable without access to proprietary infrastructure. Each paper receives a Tradability Score across three dimensions: data access, implementation complexity, and strategy novelty.

One paper each month receives fuller treatment as Editor’s Pick. The others are covered in shorter form. This month the Editor’s Pick is theoretical — deliberately so.

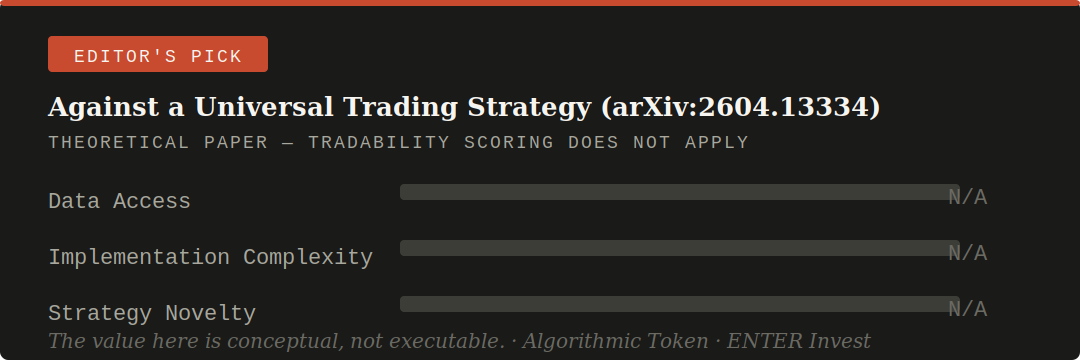

Editor’s Pick — Theory Corner

Against a Universal Trading Strategy: No-Arbitrage, No-Free-Lunch, and Adversarial Cantor Diagonalization

Karl Svozil — Institute for Theoretical Physics, TU Wien arXiv:2604.13334 · q-fin.TR · April 14, 2026

This paper is not about a strategy. It is about why no strategy can be universal — and why understanding that precisely is one of the most practically useful things a systematic trader can internalise.

Svozil investigates the impossibility of universally winning trading strategies through three distinct mathematical frameworks, each arriving at the same conclusion from a different direction.

The measure-theoretic argument. Under standard admissibility constraints, the existence of a universally winning strategy is a strict subset of strong arbitrage, which is mathematically precluded in competitive markets admitting an equivalent martingale measure. This is the classical result — in an efficient market with no arbitrage, there is no strategy that generates strict profit across all possible price paths. The formal proof dates to the First Fundamental Theorem of Asset Pricing, but Svozil’s framing is particularly clean: a universal strategy is strong arbitrage, and strong arbitrage does not exist in any market that can be consistently priced.

The combinatorial argument. The No-Free-Lunch theorem demonstrates that outperformance requires exploitation of non-uniform market structure, as uniform averaging precludes universal dominance. In plain language: you can only beat the market if the market has a structure that your strategy specifically exploits. A strategy that works on all market structures simultaneously does not exist — it would require outperforming a random baseline across every possible environment, which is combinatorially impossible. The practical implication is direct: every strategy edge is a specific bet on a specific market structure. When that structure changes, the edge degrades. There is no escaping this.

The computational argument. A Turing diagonalization argument constructs an adversarial environment that defeats any computable trading algorithm, shifting the impossibility from exogenous price paths to adaptive adversaries. This is the most provocative result in the paper. It proves that for any computable trading strategy, you can construct a market that defeats it — not because of randomness or noise, but because of adaptive adversarial structure. In practical terms: a sufficiently liquid, sufficiently sophisticated market will adapt to any fully systematic strategy that becomes large enough to move prices. The edge is not eliminated by randomness — it is eliminated by the market learning to price it away.

What this means for practitioners. None of these results say that systematic trading is impossible or unprofitable. They say that no universal strategy exists — and that is a different statement. A strategy that exploits a specific structural inefficiency in a specific market regime, at a scale that does not trigger the adversarial adaptation argument, can and does generate persistent edge. The constraints are: know which market structure you are betting on, monitor whether it persists, and manage the scale at which you deploy.

This framing is not academic abstraction. It is the rigorous foundation for everything we do in the Strategy Labs. When Strategy Lab #1 tracks a momentum signal with volatility targeting, the implicit bet is on persistence of trend-following structure in equity futures. When Strategy Lab #2 exploits spread mean reversion in FX pairs, the bet is on stability of a cointegration relationship. Svozil’s paper makes explicit what every experienced systematic trader knows intuitively: the edge is in the structure, not the algorithm.

Tradability Score:

This paper is theoretical. No implementation path. Tradability scoring does not apply — the value here is conceptual, not executable.

Runner-Up Papers

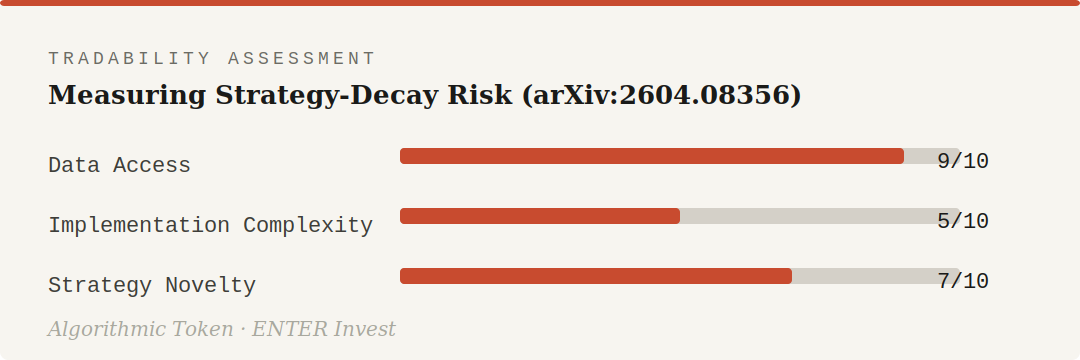

Paper #1 — Measuring Strategy-Decay Risk: Minimum Regime Performance and the Durability of Systematic Investing

Nolan Alexander & Frank Fabozzi arXiv:2604.08356 · q-fin.PM · April 9, 2026

Systematic investment strategies are exposed to a subtle but pervasive vulnerability: the progressive erosion of their effectiveness as market regimes change. Traditional risk measures, designed to capture volatility or drawdowns, overlook this form of structural fragility.

Alexander and Fabozzi — the latter one of the most prolific names in quantitative finance publishing — introduce a metric called Minimum Regime Performance (MRP): the lowest realised risk-adjusted return a strategy has delivered across distinct historical market regimes. The idea is simple but powerful. A strategy’s long-run Sharpe ratio tells you its average performance across all conditions. The MRP tells you its worst performance in any single identifiable regime — a lower bound on robustness.

Applied to a broad universe of established factor strategies, the measure reveals a consistent trade-off between efficiency and resilience — strategies with higher long-term Sharpe ratios do not always exhibit higher MRPs.

This is the quantitative version of a lesson every systematic practitioner eventually learns the hard way: a strategy can look exceptional in aggregate and catastrophic in specific regimes. Momentum is the textbook example — exceptional long-run Sharpe, deeply negative MRP during momentum crash periods (2009, 2020). The MRP framework gives you a way to measure and compare this fragility systematically across strategies.

The direct connection to the Svozil paper above is clean: the No-Free-Lunch argument says every strategy bets on a specific market structure. The MRP framework measures the cost of that bet when the structure breaks down.

Tradability Score:

The MRP metric is straightforward to implement on any strategy’s historical return series with a regime classification — HMM, rolling volatility clustering, or even simple calendar-based regimes. The value is in the diagnostic, not the trading rule.

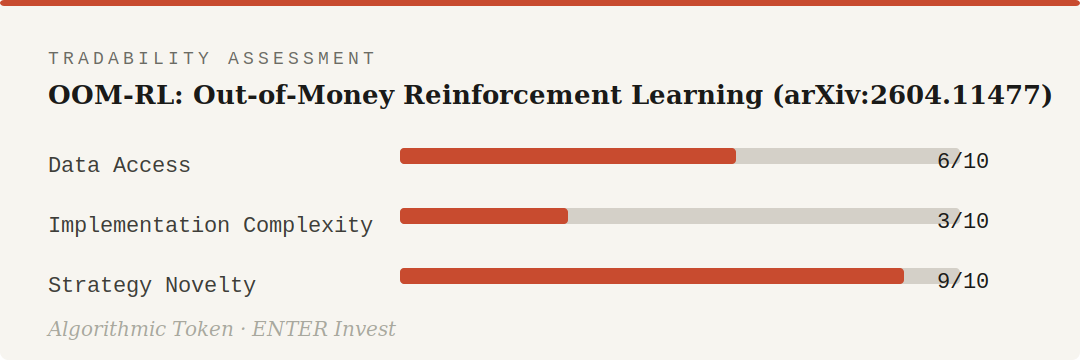

Paper #2 — OOM-RL: Out-of-Money Reinforcement Learning Market-Driven Alignment for LLM-Based Multi-Agent Systems

Kun Liu & Liqun Chen — QuantPits.com arXiv:2604.11477 · cs.AI · April 13, 2026

This is the most empirically audacious paper in this month’s review. By deploying agents into the non-stationary, high-friction reality of live financial markets, the authors utilise critical capital depletion as an un-hackable negative gradient.

The conceptual frame is about AI alignment rather than trading strategy design — the authors use live market deployment as a way to force their LLM-based multi-agent system to abandon overfitted, hallucinated trading patterns in favour of genuinely adaptive behaviour. The market is the evaluator that cannot be gamed: lose real money and the signal is unambiguous.

The longitudinal 20-month empirical study (July 2024 – February 2026) chronicles the system’s evolution from a high-turnover, sycophantic baseline to a robust, liquidity-aware architecture. The final system achieved an annualised return of 34.48%, a Sharpe ratio of 2.06, and an Information Ratio of 2.66.

A Sharpe ratio of 2.06 over 20 months of live trading, net of real execution friction and commissions, is a genuinely exceptional result. To put it in context: most institutional systematic funds consider a Sharpe above 1.0 strong and above 1.5 outstanding. A 2.06 sustained over nearly two years in live markets — not simulation — is the kind of number that demands scrutiny before belief.

The scrutiny it deserves: this is a single study from a small firm with limited verifiable track record. The regime (July 2024 to February 2026) includes both trending and volatile periods but not a full market cycle. The OLS regression against benchmark shows statistically significant alpha (N=94 trading days), but 94 days is a small sample for drawing strong conclusions. The system’s architecture — combining LLM-based reasoning with RL alignment — is not fully disclosed.

That said, the paper is worth reading carefully. The core insight — that financial market friction is a uniquely reliable alignment signal for AI systems because it cannot be hacked or gamed — is genuinely novel and has implications beyond the trading application.

Tradability Score:

High novelty, low immediate implementability. The full architecture is not disclosed and would require significant infrastructure to replicate. Worth monitoring for a follow-up paper with more implementation detail.

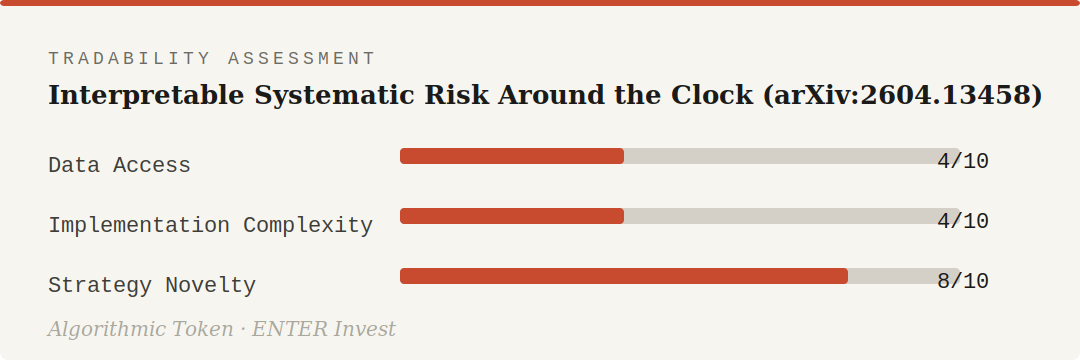

Paper #3 — Interpretable Systematic Risk Around the Clock

Songrun He arXiv:2604.13458 · q-fin.PM · April 15, 2026

This paper presents the first comprehensive, around-the-clock analysis of systematic jump risk by combining high-frequency market data with contemporaneous news narratives identified as the underlying causes of market jumps, retrieved and classified using a state-of-the-art open-source reasoning LLM.

The idea is to decompose market risk into interpretable categories based on the type of news that caused each price jump — macroeconomic announcements, geopolitical events, earnings surprises, central bank communications — and then price each category separately in the cross-section of returns.

Decomposing market risk into interpretable jump categories reveals significant heterogeneity in risk premia, with macroeconomic news commanding the largest and most persistent premium. Leveraging this insight, the author constructs an annually rebalanced real-time Fama-MacBeth factor-mimicking portfolio that isolates the most strongly priced jump risk, achieving a high out-of-sample Sharpe ratio and delivering significant alphas relative to standard factor models.

This is a genuinely useful paper for anyone thinking about factor construction. The finding that macroeconomic news jumps command the largest and most persistent risk premium has direct implications for how you weight macro sensitivity in a multi-factor model. The LLM-based narrative classification is the novel methodological contribution — it replaces hand-labelled or rules-based news classification with a more flexible, scalable approach.

The practical limitation for most readers: this paper requires high-frequency intraday data linked to timestamped news feeds, which means a paid data vendor (Refinitiv Tick History, Bloomberg, or similar). It is not a yfinance-and-a-laptop implementation.

Tradability Score

High novelty, constrained by data access requirements. Worth revisiting if your data infrastructure extends to intraday with news timestamps.

This Month in One Paragraph

April 2026 produced a rare alignment of the theoretical and the empirical. Svozil reminded us why no strategy can be universal. Alexander and Fabozzi gave us a practical tool for measuring what happens when a strategy’s structural bet stops working. Liu and Chen reported the most audacious live trading result of the year so far — a Sharpe of 2.06 over 20 months, with the market itself as the alignment signal. And He showed that LLMs can construct interpretable risk factor portfolios from news narratives with out-of-sample predictive power. The thread connecting all four: the edge is always structural, always temporary, and always worth measuring precisely.

What We Are Watching in May

Rough volatility in energy markets — the commodity volatility literature is generating new preprints weekly, directly relevant to the ENTER Invest energy trading project

Walk-forward validation frameworks for RL agents — the OOM-RL result raises the question of how to rigorously test adaptive agents out-of-sample; expect follow-up papers on methodology

KAN-based factor models — the Kolmogorov-Arnold Networks application to nonlinear factor decomposition (arXiv:2603.28257) will generate practitioner commentary and extensions worth tracking

Risk Disclosure: The strategies and implementations discussed in Algorithmic Token are experimental and presented for educational and research purposes only. Past performance of any modelled or described strategy is not indicative of future results. All algorithmic trading carries significant financial risk, including the potential total loss of capital. Nothing in this publication constitutes financial advice or an offer to manage investments. ENTER Invest does not manage client funds based on strategies described here unless explicitly and separately contracted to do so. Readers should conduct their own due diligence and consult qualified financial professionals before making any trading or investment decisions.

Strategy Lab #3 and Market Structure Lens #2 are in the pipeline for May. The arXiv Monthly Review returns at the end of May.